Have you ever stopped to think about what your financial picture truly looks like? It's almost like taking a snapshot of your money situation right now. Knowing this number, what you own versus what you owe, gives you a very clear idea of where you stand. It's a bit like getting a report card for your money, actually.

For many folks, thinking about all their money can feel a little bit messy, like a tangled ball of yarn. But figuring out this number, your personal financial standing, can be quite helpful. It lets you see if you are making progress toward your money goals, or if there are areas where you might want to make some changes, you know?

This simple number, often called your net worth, is just a way of adding up everything you have that has value and then taking away everything you owe to others. It's a basic idea, but it can show you a lot about your financial health, and sometimes, it's just good to know.

Table of Contents

- What is your financial standing, really?

- Why bother to calculate your networth?

- What bits go into figuring out your net worth?

- How do you gather the details to calculate your networth?

- The simple steps to work out your financial picture.

- Are there tools to help calculate your networth?

- What makes your financial standing change?

- A look at common mistakes when figuring out your worth.

- Keeping an eye on your financial standing over time.

What is your financial standing, really?

Your financial standing, or net worth, is a bit like a personal financial score. It is the total value of everything you possess that holds money value, minus everything you owe to other people or organizations. Think of it as a quick way to sum up your entire money situation at a specific moment. It can be a positive number, meaning you own more than you owe, or it could be a negative number, showing that your debts are greater than what you have. It's really just a simple arithmetic problem, nothing too complex, you know?

When we talk about things you possess, we mean what are often called "assets." These are items that could be turned into money, or things that represent money you have. This could be the cash in your checking account, savings tucked away, or even the value of your home or car. On the flip side, "liabilities" are what you owe. These are your debts, like what you still have to pay on your house, the money you borrowed for your car, or any balances on your credit cards. Figuring out your net worth is essentially taking one group of numbers and subtracting the other, so it's a pretty straightforward calculation.

It's important to note that this number changes. It is not something set in stone. As you earn more, spend less, pay off debts, or as the value of your things changes, your financial standing will also shift. So, it's really a snapshot, a moment in time, that gives you a useful piece of information about your money picture, like your financial health at a given point, basically.

Why bother to calculate your networth?

You might wonder why anyone would want to figure out this number. Well, for one thing, it offers a really clear picture of where you stand financially. Without knowing this, it is sort of like trying to drive somewhere new without a map; you might get there, but it will be much harder. Knowing your net worth helps you see your progress over time, which can be quite motivating, actually.

It also helps you set smart money goals. If you want to buy a house, save for retirement, or just feel more secure, knowing your current financial standing is the first step. It lets you see how far you need to go and helps you make choices that move you in the right direction. It's a bit like a personal financial report card, showing you where you are doing well and where you might need to put in a little more effort, you know?

Another good reason to figure out your net worth is for planning your future. If you are thinking about big life events, like having a family or changing careers, having a solid grasp of your money situation makes those decisions much easier. It also helps you spot potential problems early on, like if your debts are growing too quickly. So, in a way, it is a tool for better money choices, helping you feel more in control of your financial life, really.

What bits go into figuring out your net worth?

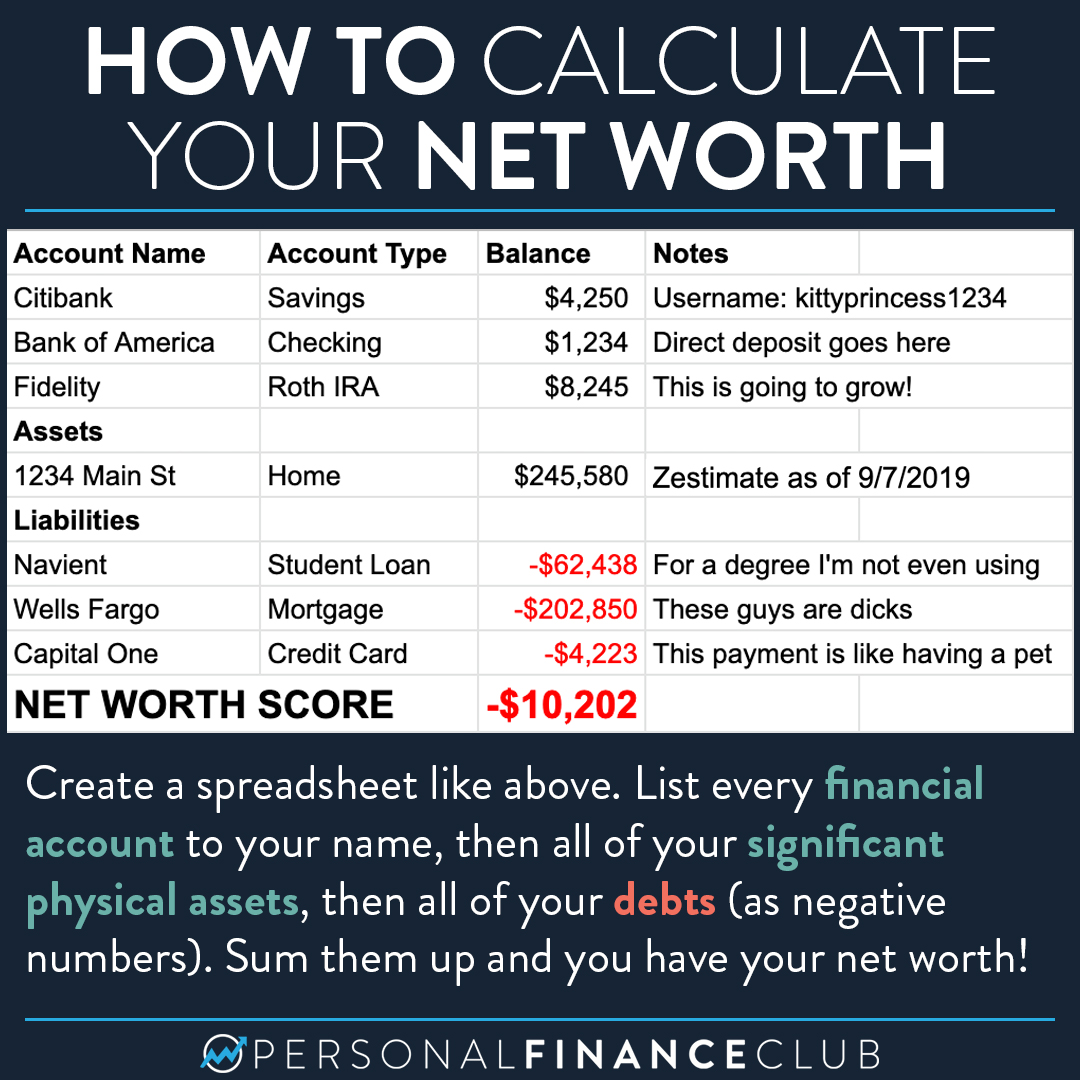

When you set out to figure out your financial standing, you need to gather two main kinds of information: everything you own that has value, and everything you owe. These are your assets and your liabilities. It is pretty simple, but getting all the pieces together can take a little bit of looking around, you know?

On the "things you own" side, you'll list things like money in your bank accounts, any savings you have put aside, and the value of any investments, like stocks or retirement funds. Your home, if you own it, is usually a big part of this. The same goes for any cars, boats, or other valuable items you possess. Even things like jewelry or collectibles, if they have significant resale value, could be included. It's about anything that could be turned into cash, or that represents money you have, basically.

Then there are the "things you owe." This includes your mortgage, if you have one, and any car loans. Credit card balances are a big one for many people, as are student loans or any other personal loans you might have. It is any money you are obligated to pay back to someone else. Once you have a clear list of both these categories, putting the numbers together becomes pretty straightforward, honestly.

How do you gather the details to calculate your networth?

Getting all the numbers together to calculate your networth might seem like a bit of a chore, but it is actually quite manageable. The first step is to pull together all your financial statements. This means looking at your bank statements for checking and savings accounts, your investment account summaries, and any statements from retirement plans you have. These papers will give you the exact figures for your cash and investments, you know?

Next, you will need to figure out the current value of your bigger possessions. For your home, you could look at recent sales of similar homes in your area or check online property value estimators. For vehicles, online guides or dealership estimates can give you a pretty good idea of what they are worth today. It is important to try and get a realistic value, not just what you paid for it, as things change in worth over time, sometimes quite a bit.

For what you owe, gather statements for your mortgage, car loans, student loans, and credit cards. These will clearly show you the outstanding balances. It is about getting a complete picture of all your debts, no matter how small they seem. Once you have all these bits of paper and numbers in front of you, you will have everything you need to start putting it all together, sort of like gathering ingredients before you cook, really.

The simple steps to work out your financial picture.

Once you have all your financial information laid out, figuring out your financial picture is pretty simple. It is a two-step process, nothing too complicated. First, you add up the value of all your assets. This means taking every single thing you own that has money value and putting it into one big total. So, all your cash, your savings, your investments, the value of your home, your car, and anything else that counts as an asset gets added up to give you a grand total, you know?

After that, you add up all your liabilities. This means taking every single thing you owe, every debt, and putting it into another big total. Your mortgage, your car loan, your student loans, and all your credit card balances go into this sum. This gives you your total amount of debt. It is important to be thorough here so you do not miss anything, basically.

The final step is to take your total assets and subtract your total liabilities. The number you are left with is your net worth. If it is a positive number, that is great! It means you own more than you owe. If it is a negative number, that just means your debts are currently more than your assets, and that is okay too, as it just gives you a starting point. The main thing is getting that number so you can see where you stand and start making plans for the future, you know?

Are there tools to help calculate your networth?

Figuring out your net worth does not have to be a pen-and-paper chore. Just like you might use a special tool to figure out dart scores quickly and correctly, or a math solver for tricky problems, there are many handy tools out there to help you calculate your networth. These tools can make the process much easier and even a bit enjoyable, honestly. Many people find that using a spreadsheet, like one from a free online office suite, is a great way to keep track of everything. You can set it up with columns for your assets and liabilities, and it will do all the adding and subtracting for you, which is pretty convenient.

Beyond simple spreadsheets, there are many free online calculators that are designed just for this purpose. Some websites, like what you might find at a place where "stuff gets calculated," offer a wide range of advanced online calculators for all sorts of things. These can often be used to figure out your financial standing by simply plugging in your numbers. They are easy to use and can give you a quick result. Some of these online tools even let you link your bank accounts and other financial accounts, which means they can automatically pull in your numbers and keep your net worth updated for you, which is very helpful, you know?

There are also many personal finance apps available for phones and tablets. These apps are often quite user-friendly and can help you keep a running tally of your assets and debts. They can also provide charts and graphs to show you how your financial picture is changing over time, which can be very motivating. So, whether you prefer a simple spreadsheet, a dedicated online calculator, or a full-featured app, there is probably a tool out there that fits your style and makes the process of figuring out your net worth much smoother, basically.

What makes your financial standing change?

Your financial standing is not a static number; it is always shifting, sometimes a little, sometimes a lot. Many things can make it go up or down. One of the biggest influences is your income. When you earn more money, and especially if you save or invest some of that extra cash, your assets naturally grow, which typically makes your net worth climb. On the other hand, if your income drops, and you have to use savings to cover your expenses, your assets might shrink, affecting your overall financial picture, you know?

Your spending habits also play a huge role. If you spend less than you earn, you have more money left over to save or pay down debts. This directly helps to increase your financial standing. But if you spend more than you bring in, you might end up taking on more debt or dipping into your savings, which would cause your net worth to go down. It is a bit like a seesaw, with what you bring in on one side and what goes out on the other, basically.

The value of your possessions also matters. For example, if the housing market goes up, the value of your home increases, which adds to your assets. The same goes for investments; if your stocks or mutual funds perform well, their value grows. However, if the market goes down, or if something you own, like a car, loses a lot of value, it can lower your net worth. Paying off debts is another big factor. Every time you pay down a loan or a credit card balance, your liabilities decrease, which directly improves your financial standing. So, it is a combination of many different things that cause your financial picture to change over time, really.

A look at common mistakes when figuring out your worth.

When you are working to figure out your financial picture, it is pretty easy to make a few common slips. One frequent mistake is forgetting to include all your assets or liabilities. People might remember their bank accounts but forget about a small retirement fund they set up years ago, or they might list their mortgage but overlook a personal loan from a family member. It is important to be thorough and make sure every piece of your financial puzzle is accounted for, you know?

Another common error is not using current values for your possessions. For instance, you might have bought your car for a certain price, but its worth today is probably much lower. Using what you paid for it instead of its current market value would give you an incorrect picture. The same goes for things like furniture or electronics; unless they are antiques or very special, their value tends to drop quickly. So, try to get the most up-to-date and realistic values for everything you own, basically.

Sometimes, people also get a bit too optimistic or pessimistic about their numbers. They might overestimate the value of their old belongings or underestimate how much they truly owe. It is important to be honest and objective when you are putting your numbers together. The goal is to get an accurate snapshot, not to make the numbers look better or worse than they are. Just take your time, gather all the correct information, and double-check your calculations, and you should be fine, honestly.

Keeping an eye on your financial standing over time.

Figuring out your financial picture just once is a great start, but it is much more helpful if you make it a regular habit. Think of it like checking your health at a yearly doctor's visit. Your financial situation changes, and by keeping an eye on it regularly, you can see how your efforts are paying off. Many people choose to do this once a month, once a quarter, or at least once a year. The frequency is less important than simply doing it consistently, you know?

When you regularly check your financial standing, you get to see trends. You can notice if your assets are growing steadily, or if your debts are slowly shrinking. This can be incredibly motivating and helps you adjust your money plans as needed. For example, if you see your net worth not moving much, it might be a sign to look at your spending or find ways to increase your savings. It is a powerful way to stay on track with your money goals, basically.

This ongoing check also helps you make better decisions for the long haul. You can see the impact of big purchases, new investments, or even changes in your income. It provides a clear, numerical way to track your progress towards financial security and freedom. So, while the first time you calculate your networth is a big step, making it a routine part of your money management is where the real benefit lies, honestly.

This article has covered what your financial standing is, why it is useful to figure it out, what pieces of information you need to gather, and the simple steps to put it all together. We also looked at tools that can help you with this task, what influences your financial picture, and some common missteps to avoid. Finally, we discussed the importance of regularly checking your financial standing to keep track of your progress.

Related Resources:

Detail Author:

- Name : Prof. Alberto Howe

- Username : fern.abernathy

- Email : ffranecki@moore.com

- Birthdate : 1971-11-20

- Address : 3592 Johnston Plains Apt. 548 Donatoville, MN 98190-4974

- Phone : 928.850.3270

- Company : Cole-Jones

- Job : Dental Hygienist

- Bio : Aliquam voluptatum aut facilis laudantium veniam quam dignissimos. Aut cumque tempora facilis molestiae ut voluptatibus. Eum fugiat amet quas quia est. Iure odio qui qui.

Socials

instagram:

- url : https://instagram.com/sadie_xx

- username : sadie_xx

- bio : Accusamus qui aut rerum ab. Ut quis et quas harum modi. Temporibus laborum sit ut omnis.

- followers : 5270

- following : 526

twitter:

- url : https://twitter.com/sadie.pfeffer

- username : sadie.pfeffer

- bio : Voluptatem fugiat sed esse corporis. Debitis voluptatem repellendus occaecati voluptas perferendis. Minus eveniet quibusdam vel reiciendis dolor.

- followers : 5354

- following : 116

linkedin:

- url : https://linkedin.com/in/sadie.pfeffer

- username : sadie.pfeffer

- bio : Vitae voluptatibus quia sint aut.

- followers : 1088

- following : 49

tiktok:

- url : https://tiktok.com/@sadie.pfeffer

- username : sadie.pfeffer

- bio : Accusantium itaque ut quia consequatur aut consectetur placeat iste.

- followers : 2992

- following : 287